Hardcover |

Kindle Edition |

Thrilling Incidents In American History |

Perry's Saints |

Prev |

Next

Hardcover |

Kindle Edition |

Thrilling Incidents In American History |

Perry's Saints |

Prev |

Next

The Jet MakersThe Aerospace Industry from 1945 to 1972• Title • Introduction • Preface • Acknowledgements • I: World War II: Aviation Comes of Age • II: The Aerospace Industry since World War II: A Brief History • III: The National Military Strategy: Background for the Government Markets • IV: The Principal Government Market: The United States Air Force • V: The Other Government Markets: The Aerospace Navy, the Air Army, and NASA • VI: Fashions in Government Procurement • VII: The Heartbreak Market: Airliners • VIII: Design or Die: The Supreme Technological Industry • IX: Production: The Payoff • X: Diversification: The Hedge for Survival • XI: Costs: Into the Stratosphere • XII: Finance and Management • XIII: Entry into the Aerospace Industry • XIV: Exit from the Aerospace Industry • XV: The Influence of the Jet Engine on the Industry • Notes • Acronyms • Annotated Bibliography |

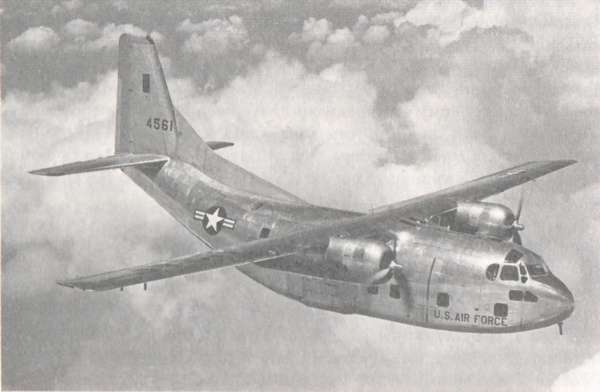

XIIIENTRY INTO THE AEROSPACE INDUSTRYThe circumstances surrounding entry of new firms into the aerospace industry provide valuable insights into the nature of the industry. What are the incentives to enter? The classical economic reason would be that profits are high and therefore attractive. A possible variation on this would be the motive to escape partly or wholly from dependence on the commercial market so as to have assured, if lower, profits. Entry could be a means to acquire technological skills at government expense, or to exploit knowledge already gained by a firm, or to bring ideas to fruition. Firms might enter to diversify so as to expand or to gain counter-cyclical insurance. Finally, entry could be attempted in order to use a firm's excess capacity.BARRIERS TO ENTRYThe value of such advantages must be large enough to make up for the cost of breaching the barriers to entry. Discussion here will be limited to entry into prime contractor status, which is critically different in composition and scale from entry at the subcontractor level. To become a prime contractor, a firm must convince a government agency that it has the best proposal among several offered. This means winning against companies with which the agency is familiar and which have demonstrated capability. The nature of this problem is best shown by the struggle by Boeing to overcome Douglas' reputation in airliners, and on an everyday basis by customer acceptance of brand names. If Boeing had this trouble with businessmen, it can be imagined how difficult it is to be in the same position with a government agency. The bureaucrats must be assured that the facilities are of adequate size, the technical and managerial staff large and skilled, and the financial resources ample. It must be acknowledged that bureaucrats run personal risks by accepting a new firm over an experienced one. If the contract runs into difficulty criticism will be certain and, since time is critical in defense projects, there will be added reproaches on this score.Some chance to by-pass competition is available through one of the exceptions to advertised bids which Congress has allowed. Negotiated contracts are permitted by these exceptions, and they form a large share of business done, especially with primes. There are seventeen exceptions: (1) a national emergency; (2) public exigency that will not allow delay; (3) purchases for less than $2,500; (4) procurement of personal or professional services; (5) the services, of educational institutions; (6) purchases made outside the U.S.; (7) procurement of medicines or medical supplies; (8) supplies bought for authorized resale; (9) subsistence supply purchases; (10) supplies and services for which it is impractical to secure competition by formal advertising; (11) research, developmental or experimental work; (12) classified purchases; (13) purchase of technical equipment which requires standardization; (14) technical or specialized supplies requiring substantial initial investment or extended period of preparation for manufacture; (15) negotiation which follows advertising; (16) purchases in the interest of national defense or industrial mobilization; and (17) exceptions otherwise authorized, such as for Congress' politico-social objectives. The tenth exception is the one most often used. The bureaucratic concern over facilities and finances is easiest to overcome because the government can still perform the role of capitalist, providing plant, equipment, and working capital if it appears desirable. There is the further assurance of the cost reimbursable contract. Herman O. Stekler estimated that if the government no longer furnished facilities, the minimum cost to build the necessary facilities to enter the space field alone was $12 million in 1965 dollars. This estimate was based upon Grumman's experience in diversifying into the space field.1 Whether such facilities are provided or not, they are useless without advanced technical skills, and these have been the basic key to entry into the aerospace industry. A firm must gain technical ability and then prepare proposals. Boeing spent three years acquiring the competence needed to develop the Saturn 5 first stage. Grumman spent $2 million for its research and proposals besides the sum it invested in facilities. And the money a company like Grumman must spend is probably less than for an outsider to the industry. A more definitive assessment of the degree to which technical skill is a barrier has been given in a paper by Dennis C. Mueller and John E. Tilton.2 They have broken the product cycle into four stages: innovation, imitation, technological competition, and standardization. Innovation involves a new product. Imitation comes after successful introduction, when the technical obstacles and market reaction can be estimated with a high degree of certainty. Technological competition follows the major advances, and only minor improvements can be made. Standardization arrives when technological progress is slow and production methods are standardized. Mueller and Tilton found entry into the innovation and imitation stages to be easy but the move into the technological competition stage to be difficult. This is a more detailed conclusion but basically the same one drawn by Peck and Scherer in 1962.3 The reason for the difficulty is that in this stage the resources and specialization needed can be provided most easily by the larger and established companies. In the standardization period, technical skills are of little importance and the question of entry shifts almost entirely to the market, which has become so exploited that marginal profits are low. The aerospace industry probably passed through the innovation stage for military jets in the late forties, and for jetliners, missiles, space, and R&D in the early and middle fifties. The imitation phase probably covered about another five years in each case, and the industry has since been in the technological competition stage. If Mueller and Tilton are correct, the best time for entry attempts would have been before the early sixties. Their thesis that a small film can enter would seem justified on th6 basis of the success of small operations such as Dassault and Lockheed's "Skunk Works," although these have not exactly been entrants into the U.S. aerospace industry. The most striking entry success has been McDonnell, the youngest of the giants. From sales of $7 million in 1946 it grew to a peak of nearly $3.7 billion in 1968. The company was started in 1939, but in its early years it was a subcontractor. It became a prime contractor in the last years of World War II, when it undertook the development of the FH Phantom 1, the Navy's first jet fighter. Thus McDonnell entered during the innovation stage for jet aircraft, and it may be significant that the most successful aerospace firm has been in the industry only since the advent of the jet. An unsuccessful entrant in the late forties was Chase Aircraft, which had an excellent piston-engine tactical transport design, the C-123, of which over 300 were built. It has seen long service including use in the Vietnam War. But it was not Chase which got the production run in 1954; it was Fairchild. Chase tried to enter during the most difficult time for a small company, at the period of technological competition in the fading piston-engine technology. Still, the fact that the company's design was a success under the circumstances suggests that entry, and by a small firm, is possible. An interesting case in entry was that of General Dynamics when it acquired Convair in 1954 in order to diversify. It was unusual because the smaller company absorbed the larger one. In the last year of independence, General Dynamics' sales were $206 million, while Convair's were $371 million. General Dynamics before the acquisition had consisted primarily of the former Electric Boat firm. CHALLENGE FROM THE AUTOMOBILE INDUSTRYThe above entries neither threatened nor gave concern to the aerospace industry. But any move from the rich and efficient auto industry might have given the existing aerospace firms pause, especially because of the production revolution of transition from tin bending to machining. The . General Motors achievement in producing the F-84F illustrates how formidable the auto industry could have been as a competitor.

The C-123 was unique as the only significant postwar aircraft designed by a small firm. It was developed by Chase Aircraft and produced by Fairchild. Courtesy Fairchild Industries, Inc. The first serious move was made during the panic mobilization days of December 1950. At 10 A.M. on 5 December the Reconstruction Finance Corporation gave ailing Kaiser-Frazer a $25 million loan and told it to get a defense contract. At 2 P.M. Air Force Lieutenant General K. B. Wolfe informed Fairchild, by telephone, that Henry and Edgar Kaiser would be at the Fairchild plant at 10 A.M. the next day to get engineering and technical data so as to manufacture C-119's. Kaiser's role was confirmed by the Air Force on 15 December even though the company's contract proposals had not yet been received by the airmen. To understand these unusual procedures, which appear on the surface to be hastily conceived decisions and to illustrate a cavalier attitude towards Fairchild, we must put them into context. In December 1950 it was feared that World War III might be imminent and that aircraft production should be increased as much and as quickly as possible. Consideration had already been given to reopening a plant for the planned expansion of C-119 production. Kaiser had experience with aircraft manufacturing as a World War II subcontractor; it had excellent plant capacity available in the giant airplane factory at Willow Run; and it already held study contracts for building bombers. Thus the transaction made some sense in the light of the situation at the time, although there is no doubt that Fairchild was treated inconsiderately. The arrangements appeared so ill considered at the time that the trade magazine Aviation Week warned that the contract should be closely monitored, saying Fairchild could build better C-119's sooner, and forecasting that Kaiser would be a high-cost producer. The following May, Kaiser, still with an ailing auto business, bought into Chase Aircraft with the intention of remaining in the aerospace business with Chase's C-123. In June 1953 a congressional investigation was started because Kaiser's production was lagging and its C-119's were costing $1,339,000 as compared to Fairchild's $265,000. In the investigation an Air Force report which was highly critical of Kaiser's efficiency was produced, and Air Force Deputy Chief of Staff for Materiel Lieutenant General Orval R. Cook, admitted that "the Air Force is disappointed . . . in the performance of the Kaiser-Frazer operation."4 Henry Kaiser gave a spirited and able defense of his company's record, partly by drawing parallels with Ford's experience at Willow Run in World War II, but during the investigation the Air Ft>rce terminated its agreements with Kaiser for both C-119's and C-123's. The press asserted that the Air Force had ended the contracts because Congress had aired a wasteful situation; the Air Force denied this contention but offered no other explanation. With termination the investigation ceased, and so, too, did Kaiser's ill-starred attempt to enter the aerospace industry. Fairchild was given the C-123 contract. The next auto firm to become interested was powerful Chrysler, at a time when the Army was competing with the Air Force for the control of long-range missiles. The Army by-passed the Air Force's allies in the interservice rivaly, the aerospace companies, and asked only the big three automakers to bid on its Redstone-Jupiter missile. A $750 million contract was negotiated with Chlysler. Thus entry was made during the innovative stage in missiles, but it was only partial. Although the auto firm participated in the development of Jupiter from the beginning, the arrangement was basically for Army arsenal development and Chrysler production. The auto company thereby failed to acquire all the technical skills involved in being a prime in the aerospace industry, but it did make a discovery ominous to that industry: Chrysler's production skills carried over easily from autos to missile airframes. The firm's experience led it to bid for a major role in missiles and space in 1959 while the fields were still in the innovative stages. Chrysler believed it had three advantages: (1) it had by then gained more experience with large missiles than many aerospace companies; (2) it had a close relationship with the German missile and space scientists of the Army's Ballistic Missile Agency, formed during the Redstone and Jupiter missile projects; and (3) it thought its reliability performance was superior to other automakers. It formed a Defense Products Group of a hundred men, most of whom were engineers. A basic flaw in these plans was that no avionics ability was built up, the same mistake Douglas made, and Chrysler was forced into coalition bidding. Further, there may have been managerial weaknesses. Instead of conducting negotiations directly with the Army, the film found itself in competitive bidding. It lost in its efforts to get the Polaris and Minuteman projects, and its only success thereafter was to win the Saturn 1 booster contract in 1961, over companies which included Avco, Boeing, Ford, Lockheed, and Vought. The presence of Ford in the Saturn 1 competition shows interest by the second of the big three of the auto industry; and the third, General Motors, made a determined effort to win the 1958 Minuteman competition. This was the contract ultimately received by Boeing, which had anticipated the call for bids and had made extensive preparations. These attempts by the powerful and able auto companies to enter the aerospace industry might have turned out differently and resulted in a reduced share of the market by the companies who had long been in the field. That the auto firms did not enter was a combination of inefficiency or bad luck for Kaiser, concentration on production instead of systems engineering by Chrysler, and Boeing's foresight in the case of General Motors. Also, the older aerospace companies benefited by their established relations with the Air Force when the Army lost the long-range ballistic missiles mission and was no longer in the market. Each service tends to do business with firms it has grown accustomed to. Without this odd combination of events the auto makers might today have a large role in the aerospace industry, for they tried to enter it at the innovative stage. Rockwell, a diversified company with a major interest in the auto industry, entered the aerospace business in an apparently classical way, through merger with North American, as already described. But Rockwell's interest was less to invade the aerospace industry than it was to strengthen its existing lines. It hoped the marriage of North American's technological innovations with Rockwell's marketing skills would generate new commercial goods and services. Therefore Rockwell's action is something less than customary entry. CHALLENGE FROM THE AVIONICS INDUSTRYFormidable as would be any challenge from the automobile companies, the most effective threat was in fact from the electronics industry. The opportunity came with the innovation stage of missiles because that type of airframe is dominated by its avionics components. In addition, the smaller missiles can be considered as a twilight zone between armament and aerospace vehicles, as they are not clearly one or the other. They will be treated as airframes in this study because the aerospace industry viewed them as such.It was fairly easy for the avionics companies to enter because they had already held subsystem contracts. Early entrants were Hughes with its Falcon and Philco with its Sidewinder and later Shillelagh. By the sixties there were also Raytheon with Sparrow and Hawk, Western Electric with the Nike family, Bendix with Talos, and Sperry with Sergeant. These were established and able companies. Only when the avionics companies had established their foothold did the giant aerospace companies take alarm. Their answer was to counterattack, to enter the avionics field. As early as 1954 the aerospace industry had 6,200 electrical and electronic engineers, and 45 percent were working on guided missile R&D. The early avionics capability arose from the need to integrate electronic equipment into the airframe and from the initial lack of components available from electronics firms. But by 1954 Convair foresaw that an avionics capability would become a prerequisite to getting contracts as a prime, and moves were made by Convair and North American, Boeing, Northrop, and Martin to produce avionics themselves. It was at this point that the Air Force intervened to protect the electronics manufacturers by threatening retaliation against aerospace firms which produced avionics goods. The threat inhibited but did not prevent the development. Five years later the aerospace firms had over four times as many electrical and electronic engineers: 27,800. The value of avionics they manufactured was about $900 million annually, of which about $130 million represented sales to other companies. The avionics firms, then, have firmly established themselves as airframe manufacturers, but only of the smaller missiles, The giant aerospace manufacturers make the larger missiles and some of the smaller ones. Perhaps it could be said that it was the aerospace firms which entered the munitions business. But it should be noted that, to a degree, the division of the missile business is logical. The avionics firms have been limited to the small missiles in which the airframes are relatively less significant, and the large aerospace companies mostly build the large missiles in which the airframes are far more important.

In general the early attempts were all made in the initial stages of technology,

identified as the easiest time for entry by Mueller and Tilton, yet that entry

has been difficult at best. Also, the fact that the attempts are concentrated in

the fifties tends to confirm the Logistics Management Institute's and Scherer's

belief that the decade was profitable and that low profits and overcapacity

appeared in the sixties. An economist would expect entrants during an industry's

period of high profitability and an absence of them during a period of low

profitability. The reverse pattern should occur with exits from the industry.

|